H.R.1’s Changes to Non-Citizen Coverage: Frequently Asked Questions

By Patti Boozang, Elizabeth Dervan and Tara Straw / March 23, 2026

Introduction

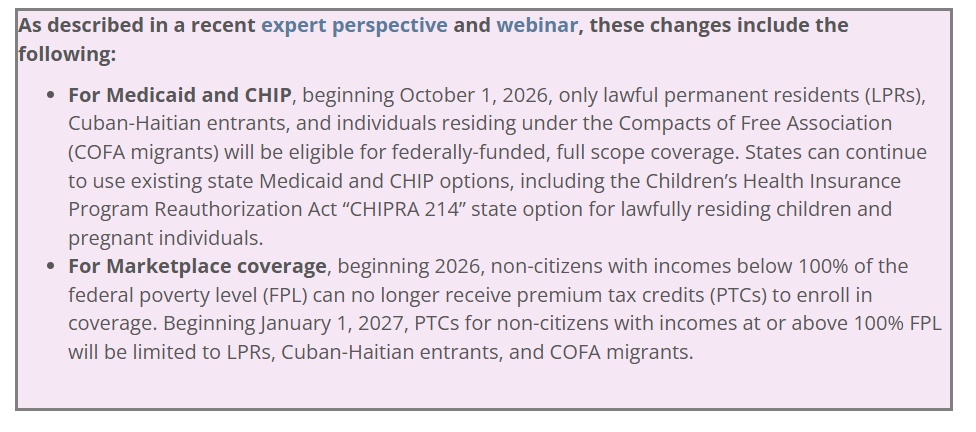

H.R.1 adds significant new limits on which lawfully present non-citizens will be able to receive health coverage through Medicaid and the Children’s Health Insurance Program (CHIP) as well as subsidized coverage through the Affordable Care Act (ACA) Marketplaces.

These changes are estimated to leave 1.3 million more people uninsured. Because immigrants are already less likely to be insured than U.S. citizens, these policy shifts are expected to widen existing health and coverage inequities affecting non-citizen communities.

This list of frequently asked questions (FAQ) is intended to serve as an added resource for states as they plan eligibility and systems updates. The Centers for Medicare & Medicaid Services (CMS) guidance implementing these provisions is forthcoming and may change the landscape further in the months ahead.

Questions and Answers

Question: How does H.R.1 affect the five-year waiting period that applies to certain non-citizens before they become elligible for Medicaid or CHIP?

Answer: Under the Personal Responsibility and Work Opportunity Reconciliation Act of 1996 (PRWORA), certain non-citizens must wait five years from their date of entry into the U.S. with a “qualified” status prior to becoming eligible for Medicaid, CHIP, and certain other federal programs.2 This waiting period is often referred to as the five-year bar. H.R.1 does not change requirements related to the five-year bar, including who is subject to or exempt from the waiting period.

In general, the five-year bar applies to LPRs (with exceptions) and certain other qualified non-citizens. Refugees, asylees, Cuban-Haitian entrants, COFA migrants, individuals granted withholding of deportation or removal, certain Ukrainian or Afghan parolees, Iraqi or Afghan special immigrant visa holders, Amerasian immigrants, veterans or active-duty service members and their families, certain American Indians born abroad, and others are exempt and may receive Medicaid or CHIP immediately.3 This exemption continues if these individuals later adjust their status to become LPRs; for example, a refugee who later becomes an LPR may continue to receive Medicaid/CHIP without the five-year bar applying.

After H.R.1’s changes take effect for Medicaid/CHIP on October 1, 2026, LPRs generally will continue to be subject to PRWORA’s five-year waiting period. Existing exemptions for people with LPR status will continue to apply, allowing LPRs who are veterans and servicemembers and their families, individuals who entered as refugees or in another humanitarian status, American Indians born abroad, and certain other LPRs to receive immediate coverage. Cuban-Haitian entrants and COFA migrants will continue to be eligible for Medicaid/CHIP coverage without a five-year waiting period.

Question: Will refugees, asylees, and others who are excluded from Medicaid/CHIP and Marketplace subsidies under H.R.1 and who later adjust their status to become LPRs become eligible for coverage? In those instances, how would the five-year bar apply?

Answer: Yes. Refugees, asylees, certain Ukrainian or Afghan humanitarian parolees, and others who will be excluded from Medicaid, CHIP, and Marketplace subsidies under H.R.1 will be eligible for these programs upon receiving LPR status, so long as they meet other Medicaid/CHIP eligibility requirements. Under current law, many of these individuals are exempt from the five-year bar and remain exempt when they become LPRs. As H.R.1 does not change how the five-year bar applies, refugees, asylees, certain Ukrainian or Afghan humanitarian parolees, and other non-citizens who are exempt from PRWORA’s five-year waiting period should be able to receive immediate Medicaid/CHIP coverage upon adjusting their status.4

Question: Are COFA migrants subject to the five-year bar to receive Medicaid or CHIP?

Answer: No, COFA migrants are exempt from the five-year bar with respect to Medicaid, CHIP, and other federal means-tested public benefits.5 While Congress initially provided COFA migrants with Medicaid coverage without the five-year bar in the Consolidated Appropriations Act, 2021 (P.L. 116-260), Congress later extended CHIP and other federal means-tested public benefits to these individuals without the five-year bar in the Consolidated Appropriations Act, 2024 (P.L. 118-42).

Question: How does H.R.1 affect people with special statuses who receive lawful permanent resident status upon admission to the U.S., such as Amerasians immigrants or Iraqi/Afghan Special Immigrant Visa (SIV) holders?

Answer: Under H.R.1, LPRs continue to be eligible for Medicaid/CHIP and subsidized Marketplace coverage. Unique requirements may apply to specific immigration statuses. For example, Amerasian immigrants are generally admitted to the U.S. as LPRs, allowing them to continue receiving Medicaid/CHIP and Marketplace subsidies after H.R.1’s changes take effect. PRWORA expressly exempts these individuals from the five-year bar for Medicaid/CHIP.6 With respect to Iraqi/Afghan SIV holders, these individuals are also generally admitted to the U.S. as LPRs and are exempt from the five-year bar.7 These individuals should continue to be eligible for immediate Medicaid/CHIP coverage.8 Individuals from Ukraine or Afghanistan granted humanitarian parole would no longer be eligible for Medicaid, CHIP, or Marketplace subsidies after H.R.1 is implemented, unless and until they adjust their status to become LPRs.

Question: Will H.R.1’s changes to Medicaid/CHIP take effect on October 1, 2026, or can states implement these changes as people come up for renewal?

Answer: H.R.1 changes the availability of federal Medicaid and CHIP funding effective October 1, 2026. This change will apply to individuals enrolled as of that date as well as new applicants for coverage. The law does not provide for a transition period. CMS guidance may provide additional detail as to how states will be expected to operationalize this change.

Question: Would individuals who lose eligibility for Medicaid/CHIP coverage or Marketplace subsidies be eligible for federally-funded emergency Medicaid?

Answer: States must provide Medicaid coverage for emergency medical services provided to individuals who would be eligible for Medicaid but for their immigration status. Individuals who would qualify for CHIP or Marketplace subsidies but would not qualify for Medicaid are not eligible for federally-funded emergency Medicaid.

Question: Can states continue to use existing Medicaid or CHIP state options to provide coverage to additional non-citizens? Who is eligible for coverage through these options?

Answer: Yes. States may continue to provide (or newly elect to provide) Medicaid and CHIP coverage to certain non-citizens after H.R.1’s changes take effect through existing Medicaid and CHIP state options. This includes the state option created in Section 214 of the Children’s Health Insurance Program Reauthorization Act of 2009 (the “CHIPRA 214” state option) allowing states to cover lawfully residing children or pregnant non-citizens. Per longstanding CMS guidance, lawfully residing children or pregnant individuals include qualified non-citizens defined in PRWORA (including LPRs within their five-year waiting period as well as refugees, asylees, humanitarian parolees, others), non-citizens with a nonimmigrant status (e.g., a work or student visa), non-citizens paroled into the U.S. for less than one year (with exceptions), and individuals with Temporary Protected Status, an approved visa petition or with a pending application for adjustment of status, among others.9

In addition, states may continue to elect to provide CHIP coverage for pregnancy-related services regardless of a pregnant individual’s immigration status through the From-Conception-to-End-of-Pregnancy (FCEP) state option. H.R.1 also does not affect CHIP Health Services Initiatives, allowing states to continue using these programs to extend FCEP coverage into the postpartum period.

Question: How does H.R.1 affect access to the Refugee Medical Assistance (RMA) program?

Answer: The RMA program is a federally-funded program managed by the Office of Refugee Resettlement that provides temporary (currently four months) health coverage to refugees and authorized populations not eligible for Medicaid or CHIP. H.R.1’s changes to Medicaid and CHIP eligibility do not affect eligibility for the RMA for refugees and other eligible non-citizens.

Question: How many lawfully present non-citizens are estimated to lose Medicaid or Marketplace coverage due to H.R.1’s coverage restrictions?

Answer: The Congressional Budget Office estimates that about 1.3 million more immigrants could become uninsured as a result of H.R.1’s changes to Medicaid, CHIP, and subsidized Marketplace coverage for non-citizens.10 This includes 100,000 lawfully present non-citizens as a result of changes to Medicaid/CHIP, 300,000 individuals due to changes eliminating the availability of PTCs for immigrants below 100% FPL, and 900,000 individuals as a result of H.R.1’s limitation of PTCs for individuals at or above 100% FPL to LPRs, Cuban-Haitian entrants, and COFA migrants.

Question: For 2026, will a lawfully present non-citizen who applies for Marketplace coverage and attests to having annual income of at least 100% FPL need to repay the entire advance PTC if their year-end annual income is less than 100% FPL?

Answer: No, repayment would not be required in this scenario. For 2026, lawfully present non–citizens continue to be eligible for PTCs if their income is at or above 100% FPL. Regulations protect taxpayers from repayment if they enrolled in a qualified health plan and received advance PTC based on an attested income of 100% to 400% FPL, even if their year-end income falls below 100% FPL, as long as the individual met all other PTC eligibility rules.11 Beginning in 2027, a more restrictive definition of eligible non-citizens applies, permitting PTC for only LPRs, Cuban-Haitian entrants, and COFA migrants. The repayment exception would continue to apply to those specific non-citizen groups.

Question: Does H.R.1 have any implications for a state’s Basic Health Program (BHP)?

Answer: While H.R.1 does not directly modify BHP statutory provisions, there are implications for the program because states are provided funding for BHP coverage based on enrollees’ PTC eligibility. In general, the BHP funding formula for states provides a payment of 95% of the value of the PTC and cost-sharing reduction (CSR)12 for each eligible individual with income up to 200% FPL. As H.R.1 ends PTCs for lawfully present non-citizens with incomes below 100% FPL beginning in 2026, their coverage garners $0 in the state’s BHP payment formula. However, this group remains statutorily eligible for BHP coverage.13 Because of the misalignment between CMS reimbursement and the coverage requirement, in December 2025, CMS announced that BHP states can discontinue coverage for this group without penalty. Specifically, CMS said it would exercise enforcement discretion for three years (January 1, 2026 through December 31, 2028) and not take action against a state that chooses not to provide BHP coverage to lawfully present non-citizens with income below 100% FPL.14 CMS has not indicated whether it will permit a similar coverage exception beginning in 2027 for lawfully present non-citizens with income between 100% and 200% FPL who are no longer eligible for PTC but are still statutorily eligible for BHP.